Happy Hour or Last Call?

Big trucking companies are reporting big second quarter revenue and profit gains, while smaller carriers struggle in a high-cost market that is very much in flux.

Welcome to the 12th edition of The Fifth Wheel with Bill Cassidy, an occasional look at a particular aspect of trucking and transportation that’s on my mind or in the news or just caught my eye. Something of a reporter’s notebook. I’ll also post occasional insights and reflections on one of my favorite topics, transportation history.

Happy Hour: Two trucking companies, flush with cash, walk into a Wall Street bar. “We’ll each take a trucking highball,” they say, “higher revenue mixed with higher profits.” “I’m sorry,” says the bartender. “Your credit’s too good here. How about a downgrade?” Don’t laugh. Publicly owned (and some private) trucking companies are defying the prevalent economic angst and reporting double-digit gains in revenue and profit. Wall Street analysts are wondering how high these trucking companies can push revenue and profit in an economy that is slowing after last year’s overheated growth. They’re asking how these companies will fare in a “coming freight recession” or just plain recession. The trucking companies themselves don’t necessarily see a freight recession coming — at least not in 2022. They see a market that has reset itself.

“I think we're having a seasonally normal July,” Shelley Simpson, chief commercial officer and soon-to-be president of J.B. Hunt Transport Services, told Wall Street analysts this week. “This might be the first July that we've seen seasonality since COVID started. … Our customers are prepared to have a good second half.”

J.B. Hunt Transport Services’ total revenue rose 32 percent year over year in the second quarter, with operating profit up 46 percent. Intermodal loads were up 7.9 percent, dedicated loads jumped 12.5 percent, and truckloads rose 13.9 percent. Okay, if you think J.B. Hunt was an exception, Marten Transport increased revenue 41.8 percent and net income 47.8 percent year over year in the quarter. Knight-Swift Transportation Holding increased total revenue 49 percent, and truckload segment revenue 11.2 percent excluding fuel surcharges. Landstar System increased total revenue 26 percent. I could go on and on. With more truckload and less-than-truckload companies reporting earnings in the coming week, we’re likely to see more double-digit top- and bottom-line growth from trucking.

Is this sustainable? For the next couple of quarters, the answer is probably yes. Unemployment is still low. Consumers have higher wages and more money in the bank than they did before the COVID-19 pandemic. Industrial growth is still in positive territory. And there is plenty of freight on the ocean, in rail yards, or in warehouses that is going to have to be moved by truck in the second half.

That could change if unemployment suddenly leaps higher and consumers hide their wallets deep in their dressers’ bottom drawers. But that hasn’t happened yet, despite the best gloom the doom merchants can spin. The best advice for shippers is to be prepared for multiple scenarios, work closely with partners to manage costs, and if you meet a large, publicly traded carrier at a bar, let them buy the drinks.

Last Call? The hour is decidedly less happy and growing late for many small trucking firms and owner-operators locked into the shrinking spot market. Many of them are struggling to keep trucks on the road, and some are deciding to park or sell them. One large Midwest shipper told us of a 300-truck carrier that decided it would be better off selling its tractors and trailers for millions of dollars than staying in business at today’s rates. Although the shipper didn’t name the carrier, I don’t doubt him.

“We have never seen supply come out so early and appear to be coming out at the same pace, if not, maybe even faster than demand seems to be waning,” Knight-Swift CEO David Jackson said during a July 20 earnings call. “All indicators are that supply is contracting already as we speak.”

But is supply really coming out of the market, or is it just shifting from one section of the market to another? The media (to which I admittedly belong) has made much of trucking authority revocations, which FTR Transportation Intelligence says topped 6,000 carriers in June, setting a new record. These are carriers who ask the Federal Motor Carrier Safety Administration (FMCSA) to revoke their authority so they can exit the business.

However, FTR also points out that new applications for authority have been even higher than revocation numbers, with about 8,000 new applications for motor carrier operating authority in June — the lowest number since February 2021. Through the first half of 2022, more new carriers entered the market than sought an exit. Those numbers seem to be headed for a balance of sorts, with revocations gaining.

Alex Lockie, executive editor at CCJ Digital and Overdrive, last week suggested what we’re seeing is “more akin to a reallocation of resources, as nimble small trucking businesses shift approach with the winds of market change.” He and FTR’s vice president of trucking Avery Vise believe some of drivers from small carriers are leaping to take jobs with large carriers. Knight-Swift’s Jackson believes that too. “We definitely are seeing more drivers,” Jackson told the SMC3 Connections conference last month. “What we’re especially seeing are more owner-operators.

“These are individuals that went out and got their authority” in 2020 or 2021, Jackson said. “They were living on the load boards, and they're ready to come back to a bit of a safe harbor” at a large trucking company like Swift or Knight Transportation.

Without denying anyone’s pain, company failures often have more to do with individual decisions than simply the ups and downs of the market. Over-reliance on certain customers and, the sudden loss of a customer, have toppled more than one company. Failure to diversify a business as market conditions change have killed others. But what’s happening in the spot market and among small carriers isn’t black and white. As I discussed last week, some companies are leaving, some are changing, and others are expanding as severe pressure on spot rates reshapes the market.

For-hire carriers added 20,600 real (unadjusted) jobs in June after hiring 25,800 workers in May and 16,000 in April, according to the latest revised data from the US Bureau of Labor Statistics (BLS). That’s 62,400 new jobs in three months. I don’t believe these are all newcomers to the industry. More likely, there’s a shift of drivers occurring from smaller to larger carriers, as truck drivers chase freight and money.

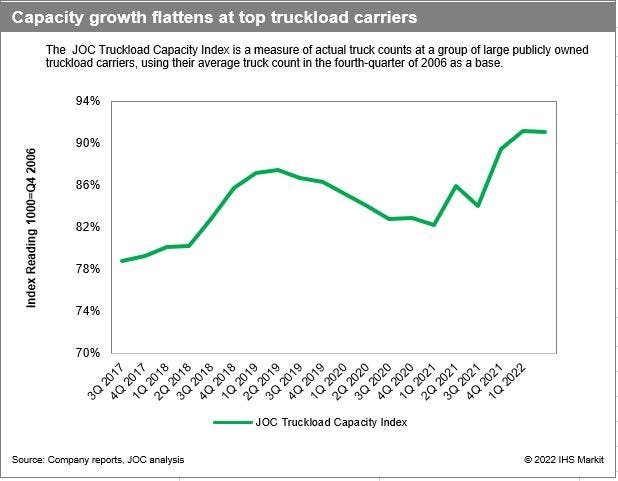

Those of us (myself included) who sit behind desks and think of our jobs as “careers” often don’t realize how often truck drivers enter, leave, and re-enter trucking, and how often they hold more than one job at the same time. They also move easily from one employer to another, or from being self-employed to being an employee. Since the 2007-2009 recession, there’s been a shift of capacity in the truckload sector from large carriers to smaller fleets (the large carriers have yet to rebuild their capacity to where it was in late 2006, according to the JOC Truckload Capacity Index, see below).

Balancing Act: Greater “balance” is returning to the truckload spot market following the first-half price correction and a shift of freight from spot to contract carriers, C.H. Robinson Worldwide president and CEO Bob Biesterfeld told Wall Street analysts Wednesday. The logistics provider’s own business is more contract now, with a 60-40 percent contract-to-spot split, compared with a 55-45 percent divide a year ago.

“The national dry van load-to-truck ratio hovered around 4:1 throughout the second quarter,” Biesterfeld said. “Between 3:1 and 4:1 for dry van is considered a reasonably balanced market versus the ratio closer to 5.75:1 that we saw in the extraordinarily tight year of 2021.” To me, a 1:1 load-to-truck ratio sounds balanced, and 3:1 or 4:1 sounds like strong demand and tight capacity — but trucking math is different.

Thanks to the sequential drop in spot market truckload rates, excluding fuel surcharges, in the second quarter, C.H. Robinson’s average truckload linehaul rate paid to carriers fell 5 percent year over year. However, the average linehaul rate billed to shippers rose 1.5 percent, excluding fuel surcharges, “supported by our contractual truckload portfolio that was negotiated in prior quarters.”

Chart of the Week:

Since the end of the so-called “Great Recession” in 2009, I’ve maintained a Truckload Capacity Index (TCI) based on actual truck counts at large, publicly owned motor carriers (the carrier group involved has more than $10 billion in annual revenue and more than 20,000 Class 8 tractors). While truckload executives talk of the difficulty of acquiring new trucks, they did build up their overall truck capacity in 2021, pushing the TCI up from 85.9 in the first quarter to 91.2 in the fourth quarter.

That indicates those TCI carriers are about 10 percent short of the capacity they had at the end of 2006, before the inventory correction, freight recession, and recession of 2007-2009. Still, the 91.2 reading in the fourth quarter was the highest since 2008.

That underscores the shift of capacity away from large carriers to smaller carriers in the past decade. The large truckload carriers that built up their fleets in the 2004-2006 trucking boom did not rebuild those fleets completely between 2009 and 2020.

In the first quarter this year, the index reading fell to 91.1. Although the data required for the index isn’t complete, a preliminary reading shows truck counts at the TCI group rose 2 to 2.5 percent from a year ago, so I believe the index likely rose again in the second quarter — most likely to a new ceiling, spurred by the transfer of drivers and capacity from the small carrier market to larger carriers mentioned above.

We’ll know in early August.

Here are some recent stories of interest from myself and my colleagues at JOC.com:

US LTL trucking ‘in a good spot’: ODFL CEO (Cassidy, July 27, 2022)

Truckload executives see US capacity under pressure (Cassidy, July 27, 2022)

BNSF, UP metering inland containers from LA-LB (Ashe, July 25, 2022)

US trucking looking more ‘seasonal’ to motor carriers (Cassidy, July 26, 2022)

Looking further afield, I recommend:

A railroad strike would swamp trucking (John Bendel, contributing editor at large, Land Line, July 27, 2022)

A national railroad strike isn’t likely, despite the vote this month in favor of a strike by the Brotherhood of Locomotive Engineers and Trainmen. But John Bendel, whose work I’ve followed since my early days at Fleet Owner, talks to folks who know how damaging such a strike would be and provides historical background well worth reviewing.

JOC INLAND: If you enjoy The Fifth Wheel, please attend the JOC Inland Distribution Conference from Sept. 26 to Sept. 28 at The Westin Chicago River North.

Thanks for subscribing to this newsletter. For those that don’t know me, I’ve been the senior editor for trucking and domestic transportation at The Journal of Commerce and JOC.com since 2009. Before that, I spent 13 years as managing and executive editor at Traffic World, a weekly magazine once owned by the JOC. I got my start in this business with Fleet Owner, a monthly magazine then owned by McGraw-Hill.

I can be reached at bill.cassidy@ihsmarkit.com, on Twitter at @willbcassidy, and on LinkedIn.

And please follow my colleagues Ari Ashe (Please Haul My Freight), Eric Johnson (The LogTech Letter), and Cathy Morrow Roberson (Rethinking Supply Chains) on Substack and on LinkedIn (where you can subscribe to Cathy’s weekly Freight Forward).

Any opinions in this blog represent the author’s views, not the Journal of Commerce, IHS Markit, or S&P Global.