Ups and Downs

No shortage of trucks on I-95; a tale of three truckers; and why the producer price indexes are so important to shippers.

Welcome to the 11th edition of The Fifth Wheel with Bill Cassidy, an occasional look at a particular aspect of trucking and transportation that’s on my mind or in the news or just caught my eye. Something of a reporter’s notebook. I’ll also post occasional insights and reflections on one of my favorite topics, transportation history.

On the Road Again: I’m writing today from my “remote-remote” office in Jensen Beach, Florida. Despite the economic slowdown and price of diesel, there were plenty of trucks on I-95 this past weekend (and the price of gas didn’t seem to have kept motorists, including myself, from getting on the road). Some of the usual suspects — long-haul truckload carriers Schneider, J.B. Hunt, Werner, Swift Transportation — were all in attendance, but so were scads of owner-operator-driven trucks and small fleets. Big G Express (Shelbyville, Tennessee) and Galway Bay Transport (Arundel, Maine) were among the many carriers sharing the road on my journey south.

I hope they were all making money and not just time.

What Goes Up … : The June producer price index for long-distance truckload released last Thursday by the US Bureau of Labor Statistics (BLS) declined 2.4 percent from May. That was significant for several reasons:

It was the first month-to-month decline for the index this year, a year in which spot truckload rates have dropped by double digits since January.

It confirmed reports by DAT Freight & Analytics and others that truckload contract rates are beginning to soften alongside the spot market, either through re-rating or as new contracts take effect. “You don’t see a decline in the PPI when spot rates begin falling, but you do see it when contract rates do,” Tal Dickstein, a senior economist at S&P Global, said in an interview. (note: S&P Global is the owner of The Journal of Commerce and JOC.com).

It showed how little overall impact the drop in spot rates has had to date this year on what shippers pay for trucking. DAT’s average dry-van spot rate, sans fuel, dropped 29 percent from January through June. But spot freight represents about 10 percent of truckload freight at the moment, with the rest covered by contract. Sectors such as less-than-truckload and specialized trucking continue to see rates and PPIs rise. This is something more CFOs need to realize.

Even with the 2.4 percent drop in the long-distance truckload PPI, the index was still 27 percent higher than a year ago, and 42 percent higher than in June 2018. It would take an unprecedented calamity to pull shipping costs down to where they were pre-pandemic. Logistics managers should plan accordingly.

A Tale of Three Truckers: An anecdotal break from hard numbers. A truck-driving friend recently told me of three acquaintances, all owner-operators with a couple of trucks, and how they’re coping the lower spot rates and high fuel prices of 2022.

In the heady days of 2021, they were all doing power-only work for a large carrier. This year, trucker A has sold his trucks and left the business, joining those looking for better pay elsewhere. Trucker B sold his tractors but bought two straight trucks and is doing good-paying local work. Trucker C is looking to buy at least one more truck, as he’s pulling in good money with a profitable mix of dedicated and spot freight.

The framework of that story may sound familiar, but it’s no fairy tale. My takeaway: Independent truckers are resilient and adaptable, not the passive victims ground to bits by the marketplace, as they’re sometimes depicted in the media.

Where Has All the Produce Gone?: Produce season usually gives the truckload spot market a lift in late spring, but not this year. In 2022, as Dean Croke says, the produce season “didn’t deliver” for trucking. “Weather is a big factor, long-term climate change is a big factor,” Croke, the principal analyst at DAT Freight & Analytics and a licensed owner-operator himself, said during an interview last week.

California, the source of 400 agricultural commodities and one-third of US vegetables and two-thirds of US fruits and nuts, has been hit hard by lack of rainfall. This US Drought Monitor map provides a good visual reference. “This has been the worst two-year period since 1956 in California in terms of drought,” said Croke. “Water restrictions and lack or rain lead to fewer crops being grown.”

Add a cold start to the growing season in the Southeast “and that’s why produce volumes are down” from previous years, he said. “A lot of carriers look to make good money out of California during produce season, and that wasn’t there for them this year.” There’s not as much livestock or red meat and poultry moving either, with more meat in cold storage, he said. “If there’s more meat and poultry in cold storage, there’s less moving in trucks.” Cold-storage volumes aren’t yet at pre-pandemic levels, he said.

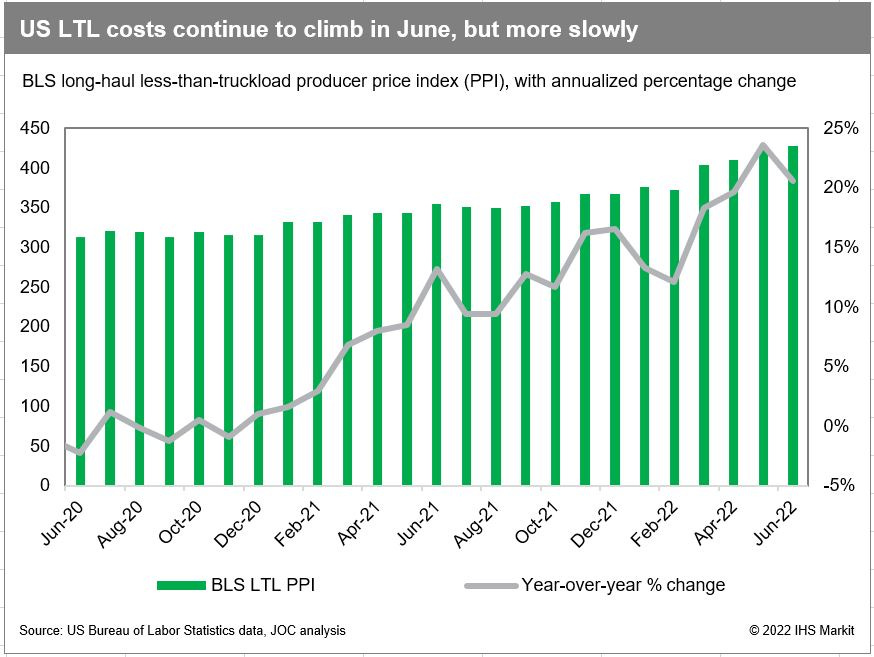

Chart of The Week:

The US long-distance, LTL producer price index for June confirmed what I’ve been hearing from LTL executives: less-than-truckload rates continue to rise, though not at the double-digit pace we saw in 2021, as capacity remains tight and underlying operating costs are well above pre-pandemic levels. The LTL PPI index rose 0.9 percent in June, following a 3.4 percent increase in May and 1.7 percent gain in April.

Here are some recent stories from myself and my colleagues at JOC.com:

Trucking PPIs indicate ‘cooling’ contract pricing (Cassidy, July 15, 2022)

Biden appoints Emergency Board to intervene in rail negotiations (Griffis & Ashe, July 15, 2022)

US truck demand rising despite slowing economy (Cassidy, July 12, 2022)

West Coast labor talks drive trans-Pacific share gains at East, Gulf coast ports (Mongelluzzo, July 15, 2022)

JOC INLAND: If you enjoy The Fifth Wheel, please attend the JOC Inland Distribution Conference from Sept. 26 to Sept. 28 at The Westin Chicago River North.

Any opinions in this blog represent the author’s views, not the Journal of Commerce, IHS Markit, or S&P Global.

Thanks for subscribing to this newsletter. For those that don’t know me, I’ve been the senior editor for trucking and domestic transportation at The Journal of Commerce and JOC.com since 2009. Before that, I spent 13 years as managing and executive editor at Traffic World, a weekly magazine once owned by the JOC. I got my start in this business with Fleet Owner, a monthly magazine then owned by McGraw-Hill.

I can be reached at bill.cassidy@ihsmarkit.com, on Twitter at @willbcassidy, and on LinkedIn.