Where has the tonnage gone?

Despite a tight-capacity trucking market and skyrocketing imports, truck tonnage is lower than it was in 2018 and 2019. MSU's Jason Miller helps explain why.

Welcome to the eighth edition of The Fifth Wheel with Bill Cassidy, a weekly (at least in theory) look at a particular aspect of trucking and transportation that’s on my mind or in the news or just caught my eye. Something of a reporter’s notebook. I’ll also post occasional insights and reflections on transportation history. I’ve been away from the desk lately and then swamped on my return, so I’m playing a bit of catchup this week with this newsletter.

Truck capacity is tight as a clam. The number of ships sitting off US ports waiting for a berth keeps hitting new highs. Intermodal service is being “metered” as demand swamps railroads. But truck tonnage, we learned Tuesday during the JOC Inland Distribution webcast, is lower than it was two or three years ago — at least that was the case from May through August, according to Michigan State University.

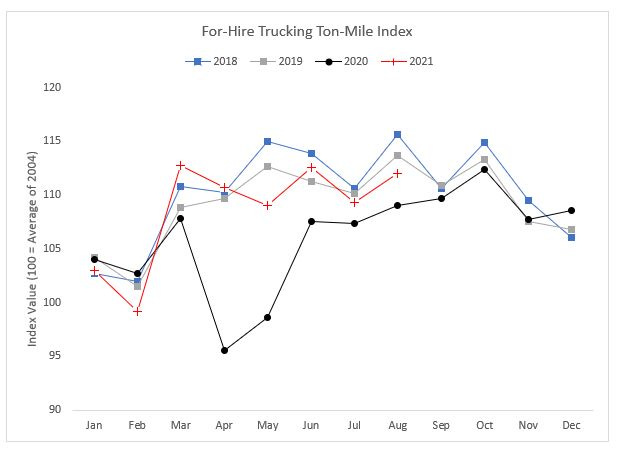

MSU’s For-Hire Truck Tonnage Index in August was down about 1.8 percent from its peak in the second quarter of 2018, Jason Miller, associate professor of logistics at MSU, told the Tuesday JOC Inland webcast — the first of three this week.

Imagine what our supply chains would look like today with more tonnage. Could we handle more cargo, in today’s disrupted, dislocated transportation market? Or is that disruption the reason we have lower truck tonnage today than in 2019 or 2018?

Here’s a chart Miller shared on LinkedIn Wednesday:

You can see that truck tonnage is higher this year than last, though the gap with 2020 is narrowing, reflecting the strength of last year’s second-half recovery. But March and April were the only months when truck tonnage topped 2018 and 2019 levels.

In the midst of the double-digit year-over-year growth in imports reported by The Journal of Commerce and others, how can that be? I’ll give you two reasons. First, we’re still in a cycle of continuous supply chain disruption caused by the COVID-19 pandemic. Shipping delays and shortages of components such as semiconductors are pulling down overall truck tonnage numbers, a point stressed in recent reports from American Trucking Associations (ATA) chief economist Bob Costello.

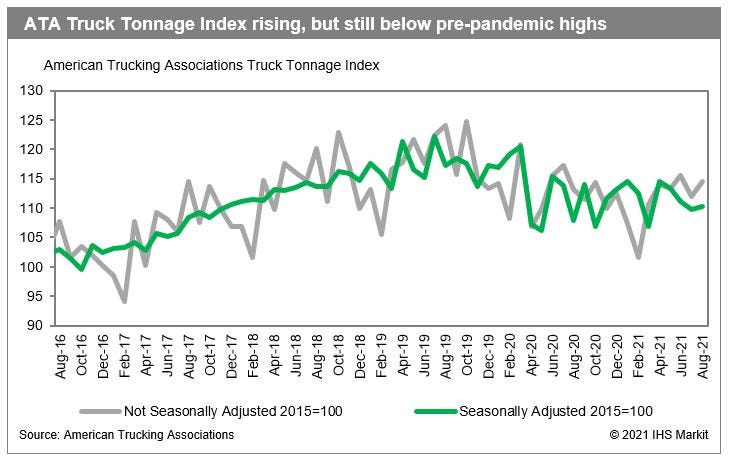

ATA’s index also shows tonnage rising, but not as high as its latest watermarks.

The second reason is that important as imports and global container shipping are to the US economy, and to trucking, they’re only part of a bigger story. The majority of tonnage moved by truck here originates within the US, with manufacturing and mining accounting for approximately 65 percent of US for-hire truck tonnage, based on the 2017 Commodity Flow Survey (US Census Bureau), according to Miller.

That’s almost heresy coming from a JOC reporter, but it’s true.

“Even though we focus so much on retail freight, that's still a smaller component of overall demand for trucking,” Miller said. However it is a component of overall tonnage that is growing, while manufacturing and mining tonnage have been falling.

“The nature of demand has changed, post-COVID,” Miller said. In the period from March through August 2021, retail-related tonnage was up 5.4 percent compared with the same period in 2018, while manufacturing-related tonnage dropped 4.9 percent, he said. “You’re essentially looking at a 10.3 percentage point spread in growth between the two sectors,” Miller said. So fewer manufacturing shipments — and energy-related shipments — mean less total truck tonnage and available freight.

“That matters because trucking companies have to balance freight networks to work efficiently,” he said. “If manufacturing shipments are down (from 2018 and 2019), it makes it harder for those small carriers that are very much organized around a manufacturing head-haul to get backhauls and get drivers back to their domiciles.” Truck capacity has been reallocated and thereby dislocated, he said.

That reallocation won’t reverse itself quickly, but if consumer spending falls as predicted in 2022, and manufacturing output rises, shippers may see further shifting of supply that changes the transportation capacity and pricing equation. The US manufacturing sector is running hot, with demand far outstripping production capacity, according to the latest IHS Markit Purchasing Managers Index.

When or if supply chain constraints finally ease, pent-up manufacturing demand will put more freight on the docks. And that could keep capacity tighter than expected in 2022. For now, “I don't see prices coming down like they did in the back half of 2018 and certainly 2019,” Miller said. “The recipe just isn't there from a capacity side.”

Here are some related articles from myself and my colleagues:

Little relief seen for US domestic shippers in 2022 (Oct. 12, 2021)

Trucking loses jobs amid transit, warehousing gains (Oct. 8, 2021)

Supply chain disruption drags truck, trailer capacity into 2022 (Sept. 27, 2021)

Import ‘flood,’ port congestion send outbound LA truckload rates skyward (Sept. 24, 2021)

Manufacturing recovery challenges US LTL capacity (April 1, 2021)

If you like this newsletter, you’ll love Please Haul My Freight, a Substack newsletter from my esteemed colleague Ari Ashe, Senior Editor for Southeast Ports and Intermodal Rail at The Journal of Commerce/JOC.com.

You’ll also enjoy Rethinking Supply Chains by JOC Senior Analyst Cathy Morrow Roberson and The LogTech Letter from JOC Senior Editor Eric Johnson.

Thanks for subscribing to this newsletter. For those that don’t know me, I’ve been the senior editor for trucking and domestic transportation at The Journal of Commerce and JOC.com since 2009. Before that, I spent 13 years as managing and executive editor at Traffic World, a weekly magazine once owned by the JOC. I got my start in this business with Fleet Owner, a monthly magazine then owned by McGraw-Hill.

I can be reached at bill.cassidy@ihsmarkit.com, on Twitter at @willbcassidy, and on LinkedIn.