Out of the Basement

With the economic indicators pointing every which way, shippers and carriers are trying to cope with 'The Circumstances.'

Welcome to the tenth edition of The Fifth Wheel with Bill Cassidy, an occasional look at a particular aspect of trucking and transportation that’s on my mind or in the news or just caught my eye. Something of a reporter’s notebook. I’ll also post occasional insights and reflections on one of my favorite topics, transportation history.

APOLOGIES: It’s been a long time since I last published The Fifth Wheel, more than six months, in fact. For personal and professional reasons I had to cut back this year on what could be called “extracurricular” writing. I’ve been encouraged to resume lately by the success of my colleagues Ari Ashe (Please Haul My Freight), Eric Johnson (The LogTech Letter), and Cathy Morrow Roberson (Rethinking Supply Chains) on Substack and on LinkedIn (where you can subscribe to Cathy’s weekly Freight Forward).

I intend to make this newsletter more a reporter’s notebook along the lines of Please Haul My Freight rather than an in-depth opinion column, with more notes and reflections on my stories on JOC.com and The Journal of Commerce.

RECESSION … OR NOT: Everyone is bracing for a recession, but who gets to call it? Not me, not you, but the National Bureau of Economic Research (NBER) Business Cycle Dating Committee, that’s who. And the NBER takes more factors than US real GDP into consideration. “The idea that two consecutive quarters of GDP contraction spell a recession is kind of an urban myth,” Jason Miller, associate professor of logistics at Michigan State University said in an interview this week. “They put a lot of emphasis on personal income and payroll employment.”

And it can take some time for the committee to make its call. For instance, the committee called the June 2009 end of the so-called Great Recession in September 2010. If we do fall into a recession in 2022 or 2023, it may be over before it’s officially declared. In the NBER’s own words: “The committee refers to a variety of monthly indicators to choose the months of peaks and troughs. It places particular emphasis on measures that refer to the total economy rather than to particular sectors.”

Those measures include monthly GDP, real personal income, payroll and household measures of total employment, and aggregate hours of work in the total economy. “The committee places less emphasis on monthly data series for industrial production and manufacturing-trade sales, because these refer to particular sectors of the economy,” according to the NBER. Read more about their method here.

‘THE CIRCUMSTANCES’: Signs are pointing to a possible contraction of US gross domestic product (GDP) in the second quarter, which ended June 30. One reason is imports, which subtract from US GDP. After all, they’re someone else’s domestic product, not ours. High levels of imports contributed to the 1.6 percent GDP contraction in Q1 2022 and may do so again in Q2.

In its July 7 US GDP tracking release, S&P Global — my employer and the owner of The Journal of Commerce — estimates that US GDP contracted 1.7 percent in the second quarter. That’s just an estimate at the moment, and it will likely change over the coming weeks. The Federal Reserve Bank of Atlanta’s GDP Now — not an official forecast but a “running estimate” — has Q2 GDP contracting 1.9 percent as of July 7.

But with the US unemployment rate in the second quarter at 3.6 percent, it’s unlikely the NBER committee will call a recession in the first half of 2022, Miller said.

I’ll follow the lead of the restaurant below and call our current difficulties “The Circumstances.”

OUT OF THE BASEMENT: Here’s what Tom Schmitt, CEO of expedited ground transport provider Forward Air, said about the odds of a recession at the SMC3 Connections conference last week:

“I think we should just be very thoughtful and careful not to panic over the next week or month or three months, that the world's going to go under and the sky is gonna fall, because it’s not. … This recession could be like a jump out of the basement, meaning short and not very deep.”

With manufacturing output and consumer spending still showing signs of growth, and US unemployment, as mentioned, at 3.6 percent (which would typically be called “full employment”), it’s hard to imagine we’re actually in a basement. We are certainly in a slowdown, what in the early 2010s was called a “soft patch.”

Inflation is considered the real culprit and the US Federal Reserve System’s interest rate hikes may turn out to be an example of how policy makers induce a recession to reduce inflation. That’s a reminder that economic cycles aren’t natural cycles or rhythms, they are created and triggered by our activity and decisions.

Economic expansions don’t simply end or die, we do something to kill them.

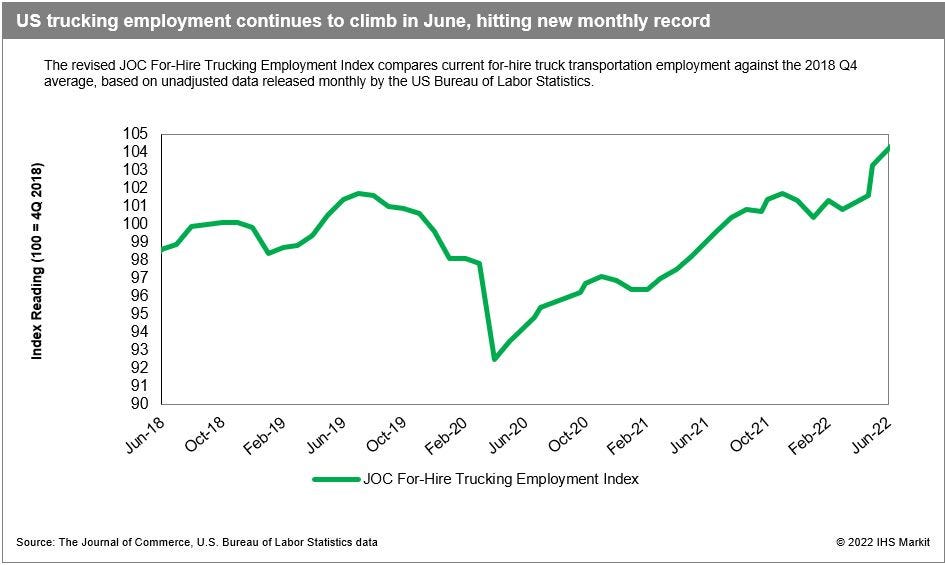

HIRING SURGE: For evidence we’re not yet in a real recession, freight or otherwise, look no further than trucking employment data released Friday. For-hire carriers have been setting new monthly hiring records of late, adding 20,600 real (unadjusted) jobs in June after hiring 25,800 workers in May and 16,000 in April, according to the latest revised data from the US Bureau of Labor Statistics (BLS).

That’s a 62,400-employee payroll gain in three months, better than even the 37,800 employees added from April through June in 2020, when trucking first began to bounce back from job losses during the early days of the pandemic. It tops the 33,800 real jobs added in same period of 2018, the previous peak year for trucking.

Trucking companies simply would not hire at this pace if they saw a sudden collapse in the US economy and freight demand dead ahead. The hiring gains underscore the strength of the contract freight market and potentially the shift of truck drivers previously working the spot market as independents back to carriers.

As David Jackson, CEO of Knight-Swift Transportation Holdings, said at SMC3 Connections last week:

“You can never say driver recruitment is easy, but it’s less impossible. We’re definitely seeing more drivers, more owner-operators...these are individuals who got their own authority and were living off the load boards and they’re ready to come back to a safe harbor.”

REAL JOBS, REAL PEOPLE: You may have noticed that I refer to “real jobs,” and that my numbers may be different from those you see in other sources. That’s because I use unadjusted employment data, not seasonally adjusted data. Without getting into a rant, I’ll say this: The reporting of seasonally adjusted employment numbers as if they reflected a real gain or decline in jobs is just WRONG. Seasonally adjusted numbers are meant to better convey long-term trends by eliminating seasonal peaks and valleys, but they don’t tell us how many living, breathing people actually started or lost jobs in any particular month. They often obscure true hiring numbers.

In April, for example, most publications reported that trucking added 13,000 jobs, seasonally adjusted. The actual number of new employees on the dock or behind the wheel, however, was 14,100, according to the BLS. The seasonally adjusted number actually tells us trucking added 13,000 more jobs than the 1,100 employees the BLS expected.

TRUCKING EMPLOYMENT INDEX: All that hiring is pushing the JOC’s Trucking Employment Index to new records, too, up 140 basis points in June to 104.7. The index is based on non-seasonally-adjusted data, which show that US trucking employment is now nearly 5 percent higher than its pre-pandemic peak in 2019.

LANDAIR CLOSING: New England used to have more less-than-truckload (LTL) carriers than church steeples. Remember St. Johnsbury Trucking? Now smaller LTL carriers are thin on the ground in New England. One of them, North East Freightways, doing business as LandAir in Williston, Vermont, is reportedly shutting down. The company hasn’t released a statement, but layoffs have been reported.

FreightWaves reports that private equity firm Corbel Capital Partners “pulled the plug” on the carrier. The company had 225 drivers and about 174 vehicles, according to information filed in 2020 with the Federal Motor Carrier Safety Administration (FMCSA). SJ Consulting Group estimates LandAir has about $28 million in annual revenue. In 2019, SJ Consulting Group put LandAir revenue at $50 million.

The carrier had $83 million in revenue when the FMCSA shut it down for 10 days following an audit that found driver-management related safety violations.

The loss of New England’s LandAir — no relation to Tennessee-based Landair Holdings — comes at a time when LTL carriers large and small are still reporting strong demand and sound profits. How does an LTL carrier go belly up in such an environment? Typically, it’s not the fault of the market, said Satish Jindel, president of SJ Consulting Group:

“It’s a combination of mismanagement, not investing in what the business needs, and some of that comes from not having proper pricing, so you don’t have proper revenue. Good times don’t prevent bad companies from going out.”

He pointed to the failure of Central Freight Lines of Waco, Texas, last year.

The results of bad management only get worse when operating costs such as fuel prices and driver wages begin to rise. Weekly average diesel prices in New England topped $6 a gallon in May and only dropped back to $5.91 a gallon last week.

LandAir’s freight will be quickly snapped up by other LTL carriers in the region, including Ross Express (a Pitt Ohio affiliate), Cape Cod Express, and A. Duie Pyle, as well as multi-regional carriers Yellow (formerly New Penn) and Saia.

“I don’t think there will be any negative impact for shippers,” Jindel said. “The amount of business they handled is so small shippers won’t have to worry about carriers saying ‘I can’t accept the volume of freight.’ The impact will be minimal.”

And if anyone tells you small LTL carriers just can’t make money in this market, don’t believe them. “I know at least two small privately owned carriers with at a better operating ratio than Old Dominion Freight Line (ODFL),” Jindel said. And publicly traded ODFL had a 72.1 percent operating ratio in the first quarter.

“Being small doesn’t mean you can’t make money,” said Jindel. “It’s not a function of size, it’s a function of competence.”

Here are some recent stories from myself and my colleagues at JOC.com:

Trucking makes ‘massive’ hiring gains on strong demand (July 8, 2022)

June bump in California spot truck rates not expected to sustain (July 7, 2022)

AscendTMS, electronic insurance partner aim to aid small fleets (July 7, 2022)

LTL carrier Pitt Ohio expands in Northeast with Teal’s buy (July 6, 2022)

JOC INLAND: If you enjoy The Fifth Wheel, please attend the JOC Inland Distribution Conference from Sept. 26 to Sept. 28 at The Westin Chicago River North.

Click the image for a special Fifth Wheel discount:

Any opinions in this blog represent the author’s views, not the Journal of Commerce, IHS Markit, or S&P Global.

Thanks for subscribing to this newsletter. For those that don’t know me, I’ve been the senior editor for trucking and domestic transportation at The Journal of Commerce and JOC.com since 2009. Before that, I spent 13 years as managing and executive editor at Traffic World, a weekly magazine once owned by the JOC. I got my start in this business with Fleet Owner, a monthly magazine then owned by McGraw-Hill.

I can be reached at bill.cassidy@ihsmarkit.com, on Twitter at @willbcassidy, and on LinkedIn.