It's Complicated

The availability of truck capacity varies by market and sector, making terms like "tight" or "loose" capacity less useful in a market where freight demand remains "elevated."

Welcome to the thirteenth edition of The Fifth Wheel with Bill Cassidy, an occasional look at a particular aspect of trucking and transportation that’s on my mind or in the news or just caught my eye. Something of a reporter’s notebook. I’ll also post occasional insights and reflections on one of my favorite topics, transportation history.

Capacity Quandary: Truck capacity may be loosening, tightening, or both, depending on what you ship and where. One thing is certain: truck capacity is complicated.

Truck capacity is more or less available depending on the lane, the type of equipment required, the type of freight (truckload, less-than-truckload (LTL), hazardous materials, flatbed, etc.), and labor availability by market.

We can’t talk about a capacity crunch or excess capacity in industry-wide, universal terms. We need to be market and segment specific.

Available capacity often depends on how much you’re willing to pay. Shippers “created” truckload capacity when they accepted stiff rate increases in contracts this year to ensure they will have committed capacity when they need it. Suddenly, routing guides that failed in 2021 began to work again, with primary contract carriers picking up loads almost all the time and less freight shunted to the spot market.

Voilà! Suddenly we have truck capacity. To some shippers, it must have seemed as if carriers pulled that capacity out of a top hat with the tap of a wand.

That shift to contract capacity siphoned freight away from the spot market, depressing spot rates and creating additional capacity in that corner of trucking. Shippers find themselves caught between the desire to take advantage of those lower transactional rates while keeping their contractual commitments and contractual capacity.

Demand Stays Steady: General media reports on “falling truck demand” almost always focus on the truckload spot market, which has seen demand as measured by volume fall this year, with load-to-truck ratios dropping, a sign of looser capacity or as C.H. Robinson Worldwide CEO Bob Biesterfeld puts it, a more balanced market. Overall demand for trucks has not fallen in the same manner, however.

In fact, demand hasn’t fallen on a year-over-year basis, Jason Miller, associate professor of logistics at Michigan State University, said during a JOC webcast on “The New Capacity Reality” Aug. 10. “We’re just not seeing signs of a steep drop (in demand) occurring right now,” said Miller, who produces a monthly truck ton-miles index with professor Yemisi Bolumole of the University of Tennessee.

You can see the drop from March to April, but the index was flat in May and likely rose in June, Miller said. You can also see that truck tonnage remains elevated. That’s thanks to higher industrial demand as well as consumer spending.

“Right now demand is a few percent higher than where it was back during that peak period of 2018, as well as where we were at times last year,” Miller said.

He claims his index is the most comprehensive ton-miles index out there because “it takes data from every freight-generating sector” of the US Census Bureau Commodity Flow Survey. The Census Bureau surveys 700,000 establishments to collect data, and there are 41 freight-generating sectors in the survey, according to Miller.

That level of demand, plus constraints on the addition of capacity highlighted by Mike Regan of TranzAct Technologies during the webcast, indicates capacity will remain tight in many sectors of trucking, even if the spot market gets loose as a goose. And that means shippers shouldn’t bet on big reductions in transportation rates in the next six to 12 months, though they may claw back some 2022 rate hikes.

“If you’re expecting rates to go back to where they were pre-COVID or even at the start of COVID in 2020, that’s not likely to happen,” Regan said.

Even if freight demand drops, trucking company operating costs aren’t likely to follow. Trucking companies that try to keep customers by lowering rates below their costs will come a cropper, as the English say. When that happens, there will be less truck capacity available, taking us back to square one, pushing up spot rates again.

You can view the archived full webcast via JOC.com.

‘Elevated’ Tonnage: The American Trucking Associations (ATA) reports for-hire truck tonnage in July remained “at elevated levels and increased significantly from a year earlier.” The ATA index is down from its high point (both seasonally adjusted and unadjusted) in March but well above its level in July a year ago or in the first seven months of 2021. The average index reading for the first seven months this year is 116.7, compared with 111.8 for the same period of 2021, ATA data show.

“Tonnage declined sequentially in July for only the second time during the last twelve months,” said ATA Chief Economist Bob Costello, falling 1.1 percent.

Seasonally, that’s not unusual in July, often a slower month than June. “While tonnage is much stronger than a year ago, the monthly gains have moderated as the year has gone on,” Costello said. “The combination of softer consumption of goods, home construction falling and slower manufacturing activity are the main reasons.”

Big Buys: Acquisitions were big news this week, led by Heartland Express’s breakaway purchase of CFI for $525 million, shortly after acquiring Smith Transport for $170 million. And it’s only two months since Germany’s DB Schenker acquired USA Truck for $435 million. That’s more than $1 billion in money spent on acquiring assets, drivers, customers and building scale by just two companies in two months.

There’s a lot more money changing hands, and more money out there looking for truckload and less-than-truckload (LTL) assets. RoadOne is building its transload empire, and Knight-Swift is shopping for more regional LTL providers. Overall, trucking companies with cash on hand are finding 2022 a good time to bulk up their operations by making strategic acquisitions, adding assets and services.

These types of acquisitions are happening up and down the supply chain. Hub Group "added scale” to its logistics services this week by acquiring TAGG Logistics, a provider of e-commerce, business-to-business, and omnichannel fulfillment services with more than 4 million square feet of warehousing space. Walmart is buying Delivery Drivers Inc., which providers drivers for its Spark delivery platform.

This is a year of opportunity for sellers as well as buyers. This round of acquisitions is in part about preparing for whatever may come next year, whether a recession or a rebound or something less than either of those outcomes. Companies want to make sure they have the resources and services they need to serve and keep their customers in 2023, whichever way the macro-economic winds blow.

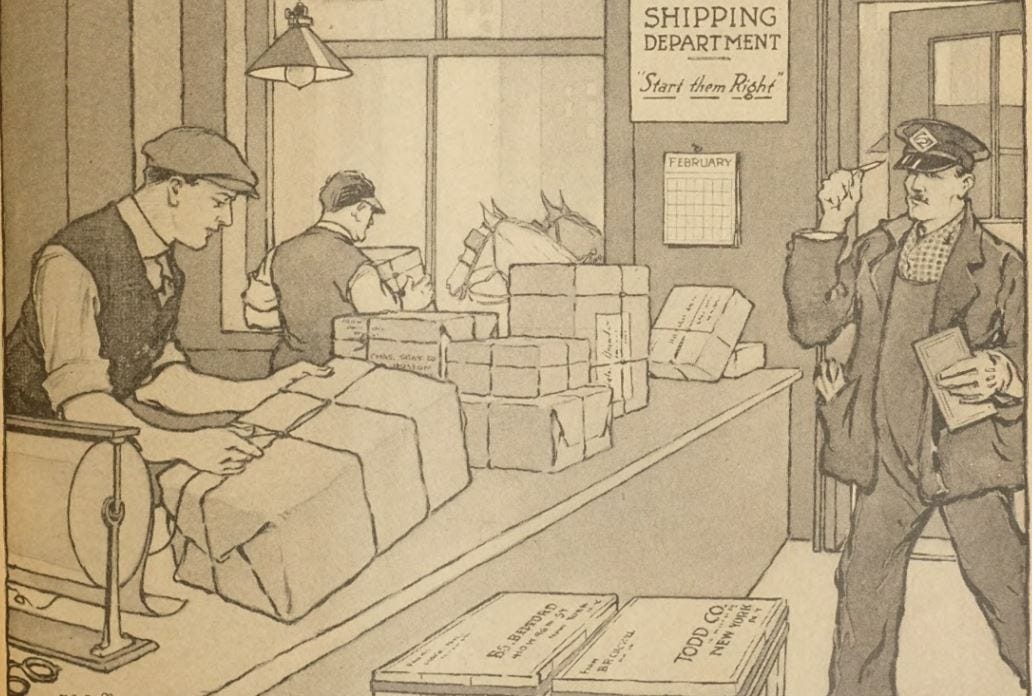

“Start them Right”

Welcome to the shipping department, 1919. These packages are being prepared for transport to the rail freight depot. Note the team of horses waiting patiently with their wagon outside the unusually large windows. The gent approaching the counter is the wagon driver (you can make out the outline of the wagon beyond the door). The badge on his cap indicates he works for the American Railway Express Company, later simply Railway Express Agency or REA. The ad this image is drawn from stated:

“A national campaign is now under way to eliminate the basic causes for many claims. These originate mainly in the shipping room and are due to poor packing and improper marking. Your shipping department can aid in this campaign by making an extra effort to see that each express shipment is started right. Will you impress upon your shipping clerks the importance of their working along these lines?”

Five score and three years later, claims are just as important to carriers and shippers as they were in 1919, as anyone who ever read the late, great Colin Barrett’s Q&A column knows. LTL claims and service issues will be discussed by a special panel at the 2022 JOC Inland Distribution Conference in Chicago, Sept. 27.

(From the March 8, 1919 edition of The Traffic World.)

Here are some recent stories of interest from myself and my colleagues at JOC.com:

Heartland doubles revenue stream with deal for CFI units (Cassidy, Aug. 22, 2022)

RoadOne adds to transload footprint in Oakland, Norfolk (Johnson, Aug. 22, 2022)

Demand drives JOC Truckload Capacity Index to record high (Cassidy, Aug. 18, 2022)

Presidential board recommends large pay hike for US rail workers (Griffis, Aug. 18, 2022)

H1 data masks big changes afoot in domestic intermodal: analyst (Gross, Aug. 12, 2022)

JOC INLAND: If you enjoy The Fifth Wheel, please attend the JOC Inland Distribution Conference from Sept. 26 to Sept. 28 at The Westin Chicago River North. E-mail me at bill.cassidy@spglobal.com for a discount code.

Thanks for subscribing to this newsletter. For those that don’t know me, I’ve been the senior editor for trucking and domestic transportation at The Journal of Commerce and JOC.com since 2009. Before that, I spent 13 years as managing and executive editor at Traffic World, a weekly magazine once owned by the JOC. I got my start in this business with Fleet Owner, a monthly magazine then owned by McGraw-Hill.

I can be reached at bill.cassidy@ihsmarkit.com, on Twitter at @willbcassidy, and on LinkedIn.

And please follow my colleagues Ari Ashe (Please Haul My Freight), Eric Johnson (The LogTech Letter), and Cathy Morrow Roberson (Rethinking Supply Chains) on Substack and on LinkedIn (where you can subscribe to Cathy’s weekly Freight Forward).

Any opinions in this blog represent the author’s views, not the Journal of Commerce, IHS Markit, or S&P Global.